Antecedent Engine — Financial Markets / First Deployment Currently deployed

Enquire about access →What is the current state of the system?

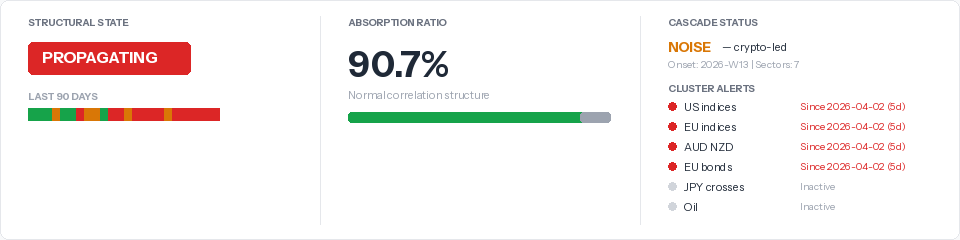

The Antecedent Engine does not predict direction. It detects when the structural state of a system is changing — before the change becomes visible to conventional indicators. The architecture is direction-agnostic: a Propagating reading does not indicate whether markets move up or down, only that a confirmed signal is spreading across correlated systems.

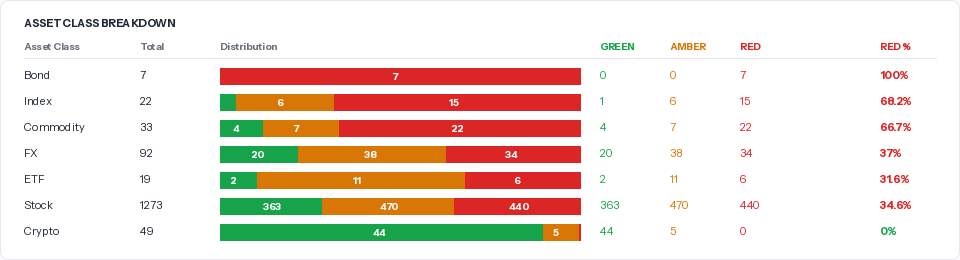

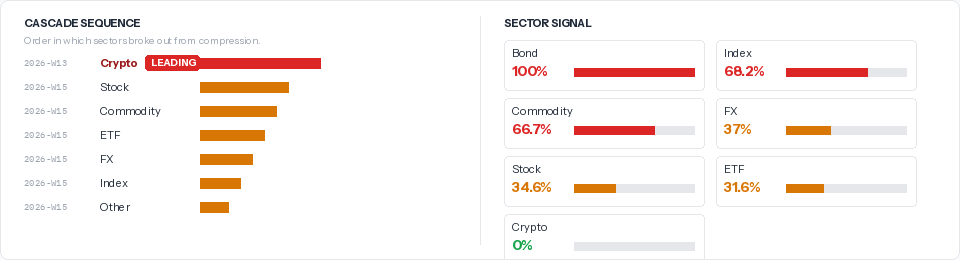

Currently deployed across approximately 1,500 instruments spanning FX, equities, indices, commodities, bonds, crypto, and ETFs. Outputs include per-instrument state classification, cluster warnings, cascade detection, and contagion mapping.

Engine v2.3 — ~1,495 instruments — Institutional access only. Not investment advice.

Most recent confirmed transition: structural tension detected 22 days before the Iran conflict escalation, April 2026. Cluster warnings, cascade sequence, and contagion mapping delivered to subscribers before conventional indicators responded.

Once a state is recorded, it does not change retroactively. The same input always produces the same output. The engine detects the weather. You decide whether to carry an umbrella.

The underlying detection architecture is domain-agnostic. Financial markets is the first deployment. If your industry requires structural state classification, get in touch.